SUMMARY

To achieve the global climate objectives outlined in the Paris Agreement, the International Energy Agency (IEA) estimates that global energy consumption must transition to net zero emissions by 2050. Models for achieving this outcome often assume a complete replacement of fossil fuels with renewable and clean energy sources, as well as vehicle electrification. Compared to traditional capital stock, these resources are much more mineral intensive. Electric vehicles (EVs) are six times as mineral intensive as an internal combustion engine vehicle, and wind turbines nine times as mineral intensive as natural gas power plants for the same capacity. This raises the possibility that high minerals demand for clean energy could lead to challenges of scarcity, creating a potential threat to U.S. energy security.

Electric vehicles (EVs) are six times as mineral intensive as an internal combustion engine vehicle, and wind turbines nine times as mineral intensive as natural gas power plants

Of special interest are minerals categorized as “critical,” defined as “essential to the economic or national security of the United States.” This white paper offers a meta-analysis of three studies from Valero et al., Dominish et al., and Månberger & Stenqvist. They estimated the total cumulative demand for critical minerals to achieve the net-zero emissions pathways as laid out by the IEA and other organizations. All studies showed unprecedented increases in mineral demand and for expected demand to exceed global reserves for cobalt and lithium.

Beyond concerns as to the feasibility of achieving the global production necessary to meet emissions reduction targets, assessment of global supply chain security reveals further complications. For most critical minerals, the United States and other Western nations are minority suppliers with only modest capability to influence global markets. By contrast, China is the dominant supplier for multiple critical minerals and is likely to remain so. In the case of minerals it does not supply—such as cobalt—China has near-monopolistic control of refining capacity through its state-owned enterprises.

China is the dominant supplier for multiple critical minerals and is likely to remain so. In the case of minerals it does not supply—such as cobalt— China has near-monopolistic control of refining capacity through its state-owned enterprises.

There are also ethical challenges associated with the production of critical minerals and associated clean energy technology that are not sufficiently addressed. In the case of cobalt, it is estimated that there are 40,000 child workers in the Democratic Republic of the Congo (DRC) mining cobalt, aged as young as six. An essential input for solar panels, polysilicon, mostly comes from the Xinjiang province of China, where an estimated one million Uyghurs have been forced into internment camps. A recent study estimated that approximately 2.6 million Uyghurs are slave laborers, many of which are likely contributing to Chinese solar panel production.

Additionally, there are economic security concerns with China’s current domination of critical minerals. In 2010, Beijing embargoed the export of rare earth elements to Japan because of tensions in the Senkaku islands, leading to speculation that continued reliance on China for critical minerals needed for U.S. energy production and elsewhere could be a security vulnerability.

To mitigate risks to the global supply chain related to critical minerals, the United States should implement policies that improve recycling and pursue breakthrough innovation for energy technology that may be less mineral intensive than currently available EVs, wind turbines, or solar panels. The United States should also implement policies that consider how increased domestic and global production of critical minerals could alleviate the national security, ethical, and environmental concerns that come with sourcing foreign critical minerals.

INTRODUCTION

There is considerable momentum behind environmental advocacy movements that call for “100% renewable energy” sourcing by 2050, net zero emissions by 2050, and similar transformational changes to reduce global greenhouse gas (GHG) emissions. Major institutions that offer policy analysis and recommendations, such as the International Energy Agency (IEA), the International Renewable Energy Agency (IREA), and the National Academies of Sciences (NAS) have all produced studies that lay out the requisite changes in capital stock to meet such objectives. Less discussed, though, are the potential physical constraints that may impede the achievability of such emissions targets, particularly those dependent on certain low-carbon technologies.

Modeling exercises assessing the costs and feasibility of transitioning entirely to clean energy conventionally rely on “capital stock rollover” models. Simply, the modeler estimates the life of existing assets, assumes they will be replaced with clean assets, and then provides an estimate of the timing and cost based on the marginal differences (in cost, cleanliness, etc.) between the reference case and the modeled case. Because these models typically assume perfect substitutability between resources, they often ignore the underlying constraints that may impede asset replacement.

In considering recent pushes for estimating the achievability of a clean energy transition on hoped-for timelines, it is worth exploring if there may be unrealized constraints that are not conventionally included in existing models. Increasingly, scholars are questioning the mineral requirements that would be needed to reach either 100% renewable or clean energy targets. For example, what if a model calls for complete electrification of light duty vehicles (LDVs)? It is estimated that by 2025, 75% of all mined lithium will be used for electric vehicles (EVs), but currently, EVs only account for 1% of global LDVs and are expected to account for just 7% of transportation by 2030. In other words, to meet the proposed emission targets, more lithium will be required than is expected to be produced, and it is unclear if the production increases at the required scale are feasible.

This analysis aims to examine existing literature and offer insight as to the total mineral requirements to reach planned emission targets. In doing so, this paper aims to establish whether there is consistency in the literature as to the estimated mineral requirements of a clean energy transition, as well as if concerns about mineral constraints are warranted.

Furthermore, this paper aims to highlight and explain potential non-energy related issues that may impede mineral allocation for climate policy purposes. This includes national security concerns and ethical concerns such as the utilization of slave labor in foreign nations.

With improved information and understanding of the minerals requirements for a clean energy transition, policymakers should be better equipped to understand the potential costs and benefits of policies aimed to address climate change, especially as it relates to 100% renewable energy mandates like those that are already in effect in several states or President Biden’s goal for half of all new vehicle sales to be EVs by 2030. Policymakers should also understand the energy security implications of policies that lean heavily on mineral-intensive products for abating greenhouse gas emissions, as scarcity of materials could raise prices as well as create dependency on foreign suppliers that could have an interest in manipulating the market.

Background

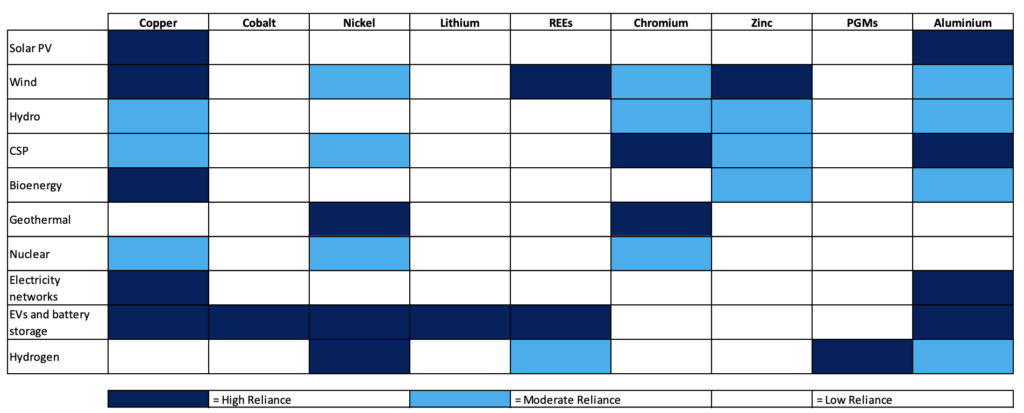

Wind turbines, solar panels, electric vehicles, energy storage, electric transmission, and other technologies utilized in a global clean energy transition require minerals—the most important of which are categorized as “critical.” These minerals are defined as “essential to the economic or national security of the United States,” and there are currently 50 listed critical minerals, up from 35 in 2018. Critical minerals represent a vulnerability due to their scarcity, high demand, and the high reliance of the U.S. economy upon them.

The intensity of mineral requirements for clean energy products can be quite substantial; the IEA notes that an EV requires 207 kg of critical minerals, whereas an internal combustion engine vehicle (ICEV) only requires 34 kg, making the EV roughly six times as mineral intensive. Similarly, an onshore wind turbine requires 10,152 kg of critical minerals, whereas a natural gas plant requires 1,148 kg, making the onshore wind turbine nine times as intensive. The IEA also notes that clean energy technologies will be the dominant source of global demand for several critical minerals by 2040, accounting for 92% of lithium, 69% of cobalt, 61% of nickel, 45% of copper, and 41% of rare earth elements. The table below highlights how these minerals are used in clean energy technology, according to the IEA.

Clean energy technologies will be the dominant source of global demand for several critical minerals by 2040.

Table 1. Critical minerals essential for key clean energy technologies.

Source: “IEA Mineral Requirements for clean energy transitions.”

In the above table, there are two noted groups of minerals that are subsets of critical minerals, rare earth elements (REEs) and platinum group metals (PGMs). Of the two, the more concerning are REEs, which despite their name are not conventionally rare but rather are rarely in concentrations sufficient for economic mining. In 2019, the Department of Defense requested plans for the increase of REE production in the United States, as an imminent risk to military procurements and supply chains due to reliance on China had become apparent.

For clean energy technology, REEs can have particular importance. For wind power, a mineral called neodymium is needed for magnets, and a wind turbine’s magnet can have a weight of up to 650 kg per megawatt of capacity; up to 29% of that content can be neodymium. For solar panels, a material called tellurium is used, and about 100 metric tons of that mineral is required for one gigawatt (GW) of solar power. REEs present a vulnerability in the pursuit of a clean energy transition because substitutes are not always available, and when possible, may not be as efficient.

While REEs may be scarce, other conventional minerals such as copper, cobalt, nickel and lithium present their own challenges due to the vast quantities needed to produce clean energy technology. Despite their relative abundance, never have they been in demand at the scale that could be required of under certain global clean energy transition pathways, raising questions as to the feasibility of such large amounts of extraction.

There is a risk of scarcity when it comes to critical minerals due to the combined enormous quantities of conventional minerals needed and the heightened demand for specific rare minerals that may lack substitutes. While it may be tempting to liken the minerals inputs for some clean energy technologies to the fuel inputs of fossil fuels, the scarcity risks are not similar. Fossil fuels are relatively abundant, with vast untapped reserves both on land and undersea, whereas novel ways of extracting critical minerals unconventionally have not yet been widely adopted.

For example, some speculate that extraction of lithium from sea water can avoid supply chain scarcity issues, but the density of lithium in seawater is very dilute at 0.2 parts per million. While it has been technically proven as possible to extract lithium in this manner, it is not yet clear if such efforts could be widely commercialized. For the foreseeable future, policymakers should assume that minerals production will be limited to conventionally established, economically viable methods of extraction.

The Clean Energy Demand for Critical Minerals

Currently, approximately 80% of global energy needs are met with fossil fuels, 5% from nuclear power, and 15% from renewable sources. Under the Paris Agreement, Parties agreed to hold the increase in the global average temperature to below 2°C above pre-industrial levels and pursue efforts to limit the temperature increase to 1.5°C above pre-industrial levels. The IEA has projected that only a 50% chance of meeting the latter goal would require global net zero emissions by 2050. For context, the IEA’s Net Zero report estimates that 70% of global electricity demand would be met with wind and solar power. The IEA’s projection also requires the nearly complete electrification of all light-duty passenger vehicles, up from the current level of less than 2% of vehicles. In all ways, the IEA modeled clean energy transition envisions a massive adoption of clean energy technologies at an unprecedented scale and is expected to be extremely mineral intensive.

The IEA estimates the total annual mineral demand required for their net zero emissions pathway to be 43 million metric tons, which is roughly six times current levels. Modeling exercises for the transition often presume that clean energy replacements of fossil fuels are readily available, and that innovation and economies of scale will cut costs. Less studied is if heightened demand for minerals would create scarcity, driving up prices and the cost of a transition.

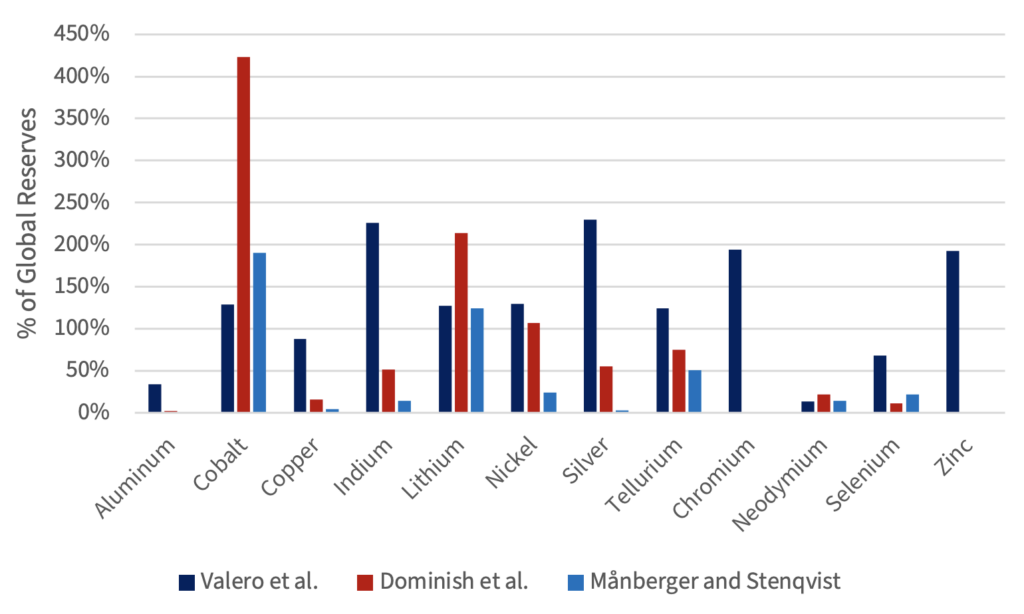

Fortunately, some studies have released data-oriented estimates of the cumulative mineral requirements for a transition. This paper references three key analyses that offered estimates of the total demand for a variety of critical minerals: Material bottlenecks in the future development of green technologies by Valero et al., Responsible minerals sourcing for renewable energy by Dominish et al., and Global metal flows in the renewable energy transition: Exploring the effects of substitutes, technological mix and development by André Månberger and Björn Stenqvist. Analysis of Potential for Critical Metal Resource Constraints in the International Energy Agency’s Long-Term Low-Carbon Energy Scenarios by Watari et al. was also used as a reference, particularly for information on rare earth reserves and resources.

Notably, there is a significant range in the estimates required across all three analyses, which can largely be attributed to varying assumptions as to the rates of improvement in the efficiency of materials utilization and in recycling, as well as the substitutability of minerals. However, all three analyses estimate a non-trivial portion of the Earth’s total critical minerals would be required to meet global clean energy demand.

The chart below outlines the total minerals needed according to each analysis, expressed as a product

of the total globally available mineral reserves.

Figure 1: Total minerals needed for a clean energy transition, as a product of the total globally available mineral reserves.

Sources: Estimates based on data from USGS Mineral Commodity Summaries 2021, U.S. Geological Survey, 1 February 2021,

https://pubs.er.usgs.gov/publication/mcs2021; and Valero et al., Dominish et al., Månberger and Stenqvist, and Watari et al.

There are multiple minerals where all three studies affirm that global clean energy demand will exceed worldwide reserves. For cobalt, Valero et al, Dominish et al, and Månberger and Stenqvist found that the energy transition would require 129%, 423%, and 190%, respectively. Similarly, all three studies expect a demand greater for lithium—128%, 214%, and 124%. For nickel, Valero et al. and Dominish et al. estimated 129% and 107% of reserves, in that order, while Valero et al. estimated the world would require 194% and 193% of its chromium and zinc reserves.

Even for minerals that did not exceed known reserves, estimated required amounts frequently accounted for substantial portions of what the world has. For example, Dominish et al. and Månberger and Stenqvist projected that 75% and 51% of tellurium reserves, respectively, would be needed.

Overall, of the 31 mineral requirement estimates we examine in this analysis, 19 found that more than half of global reserves of a specific mineral were necessary, while only three estimates were less than 10% of global reserves.

In short, the potential mineral requirements for a complete clean energy transition with existing technology is so large that it is not clear if it is economically viable to extract enough minerals to meet the needs modeled in those studies. In at least the case of cobalt and lithium, there is agreement across the three studies that currently estimated global reserves are insufficient.

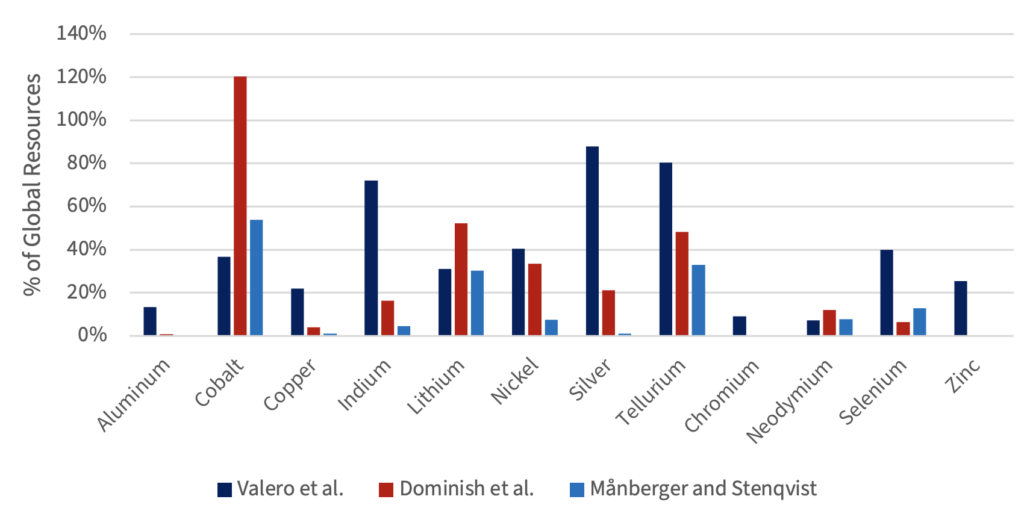

A counterpoint to such critiques, nonetheless, is that there is a large difference between reserves and what are called “resources.” Mineral reserves can be defined as the quantities that are both known and economically viable to extract, and that definition is generally the most appropriate variable for estimating available supply.

Technology improvements or the discovery of new deposits could change the estimates of available reserves. Moreover, deposits that may not have been economically viable may become accessible if prices increase. On the other hand, “mineral resources” are the estimated total physical availability of a mineral on Earth. While this term does not represent the total minerals that could be extracted today, it does represent a hope that future technology may unlock these minerals. For example, significant untapped resources of lithium exist in Bolivia, which has the largest identified lithium resource in the world, at 21 million metric tons (24% of global resources). A successful method of mining this brine-based resource hasn’t been developed yet, although pilot tests for production are underway. Currently, Australia, Chile, China, and Argentina account for most of the world’s lithium production.

The chart below applies the above estimates of mineral requirements for a clean energy transition

that and applies them to global “mineral resources.”

Figure 2: Total minerals needed for a clean energy transition, as a product of the total globally available mineral resources.

Sources: Estimates based on data from Mineral Commodity Summaries 2021, U.S. Geological Survey; Valero et al., Dominish et

al., Månberger and Stenqvist, and Watari et al.

Even with the more generous metric, minerals requirements could be considered concerning. For some minerals that may be less commonly available, such as tellurium, all three studies estimate 33% or more of global resources would be needed. Conversely, some resources that are abundant, but not economically viable to recover in all cases, such as chromium, are less of a concern. The salient takeaway is that even when considering the total volume of the world’s mineral resources, constraints for achieving a global clean energy transition with existing technology exist.

The table below summarizes the scale of the minerals needed to achieve the clean energy transition by showing the average of the three referenced studies, expressed as a percentage of total global reserves and total global resources.

Table 2: Reserves vs resources of critical minerals needed for the clean energy transition.

Sources: Estimates based on data from USGS Mineral Commodity Summaries 2021, Valero et al., Dominish et al., Månberger and

Stenqvist, and Watari et al.

It should also be noted that the above assessment is not comprehensive. There are some minerals essential to the transition, such as dysprosium, that may not be available in sufficient quantities (a rare earth of which China supplies 99%). However, due to data limitations, they were not included in this analysis.

Sourcing of Critical Minerals

Minerals Production

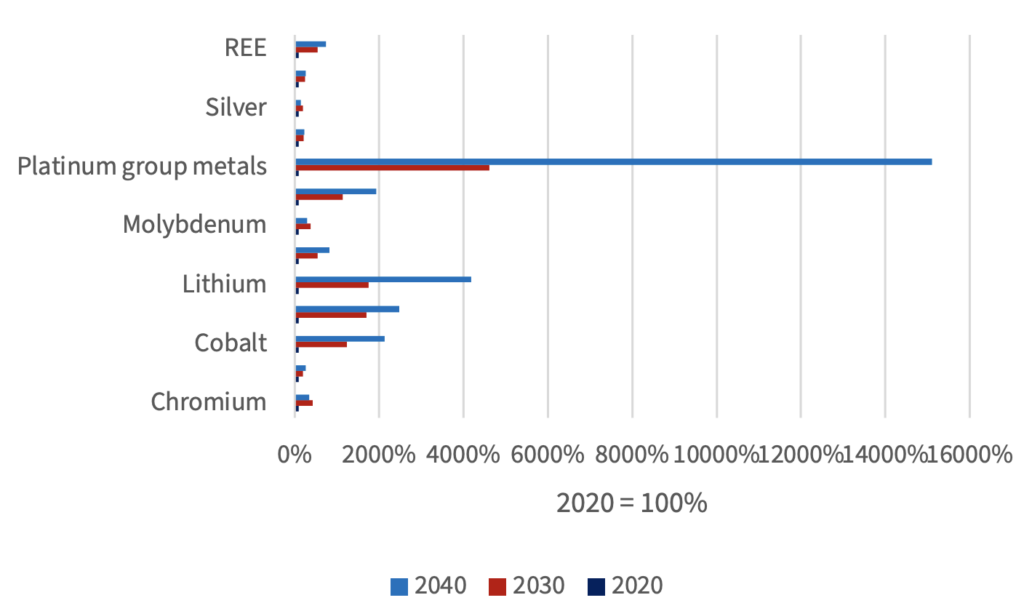

Beyond concerns about total cumulative minerals demand, there are significant potential constraints in the requisite increases of minerals production to meet long-term objectives. Current minerals production falls far short of the levels that are projected to be needed in the future, according to the IEA.

Figure 3: Required production of minerals relative to 2020.

Sources: IEA The Role of Critical Minerals in the Clean Energy Transition, May 2021.

For some minerals, the anticipated increase in demand is enormous. Lithium demand is projected to be 42 times above current levels by 2040. This raises a key question: where will production of minerals increase to meet the demand of a clean energy transition?

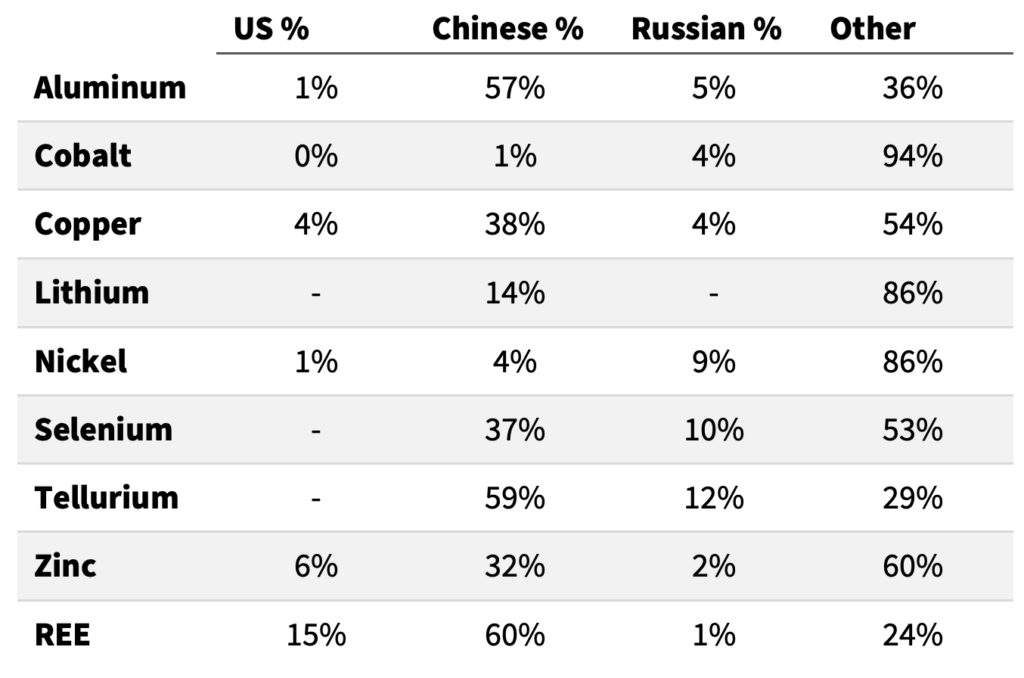

Current production of critical minerals occurs mostly outside of the United States and developed nations. The table below highlights several critical minerals and shows U.S., Chinese, and Russian production, as well as output from the rest of the world. For lithium, selenium, and tellurium, U.S. data has been withheld.

Current production of critical minerals occurs mostly outside of the United States and developed nations.

Table 3: Production of critical minerals.

Sources: USGS Mineral Commodity Survey 2022.

In all cases except REEs, U.S. production represents only a small fraction of total global production.

In all cases except REEs, U.S. production represents only a small fraction of total global production. Although not on the table, the only mineral where an OECD nation is the production leader is lithium, as Australia accounts for 55% of global production. China is the dominant supplier for 21 of the recognized critical minerals in the United States. For cobalt, the Democratic Republic of the Congo (DRC) is responsible for 71% of global production, and for nickel, Indonesia accounts for 37%. Although Russia is not a predominant supplier, it does exceed U.S. minerals production for several critical minerals.

China is the dominant supplier for 21 of the recognized critical minerals in the United States.

Because mineral extraction relies on the physical availability of mineral deposits, fungibility of suppliers may be limited. For example, the DRC is the dominant supplier of cobalt because of the unique geologic conditions of the Central African Copperbelt that makes it essentially the only major deposit of accessible cobalt. This makes it unlikely that an alternative cobalt supplier will emerge in the market, so policies that increase demand for cobalt will naturally heighten the DRC’s influence in markets consuming cobalt.

Alternative mineral deposits around the world often exist, but for sometimes artificial reasons are inaccessible. REEs are relatively common globally and are present in substantial quantities in the United States, but permitting difficulties make extraction difficult. In response to rising REE demand, old U.S. mines have restarted, but expanding extraction has been difficult. Delayed permits have at times killed projects that were no longer economically competitive because prices have fallen.

It should also be noted that where minerals are produced matters. For example, it is estimated that mining and extraction of both energy and non-energy related products in China is 2.2 times as carbon intensive as the United States, and mining support services are 5.2 times as carbon-intensive. Although this paper does not explore in depth how pollution from mining for clean energy production may have potential environmental impacts, it should be noted that existing policies may fail to consider how disparate the upstream environmental impacts are from various mineral producers.

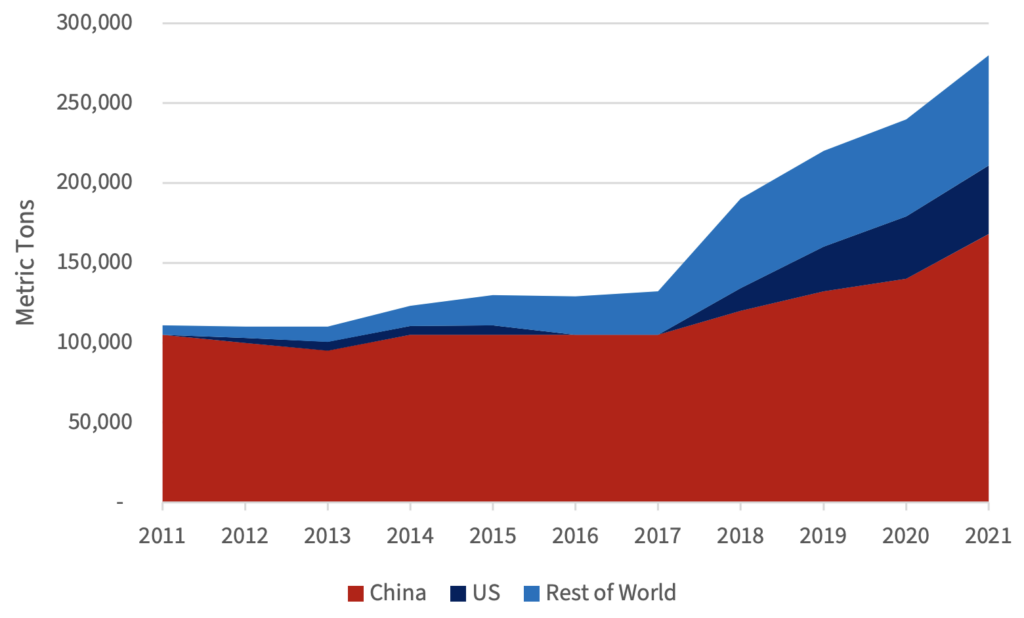

REEs offer a good example of how global production can change in response to rising demand, especially in the case of the United States, which has a national security motivation for expanding production. The chart below shows ten years of REE production, comparing the United States, China, and the rest of the world.

Figure 4: Rare earth elements production.

Sources: USGS Mineral Commodity Summaries 2013-2022 (rare earth elements).

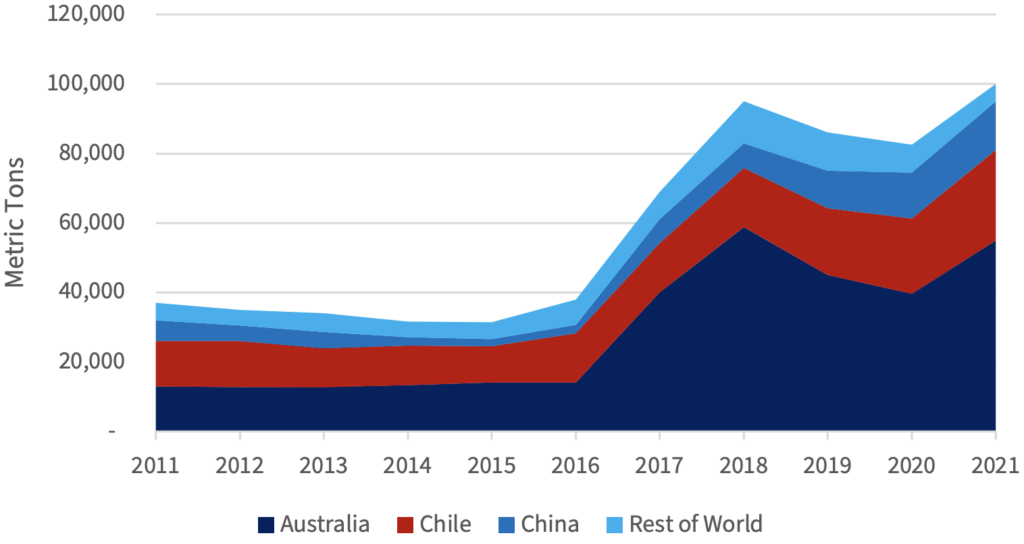

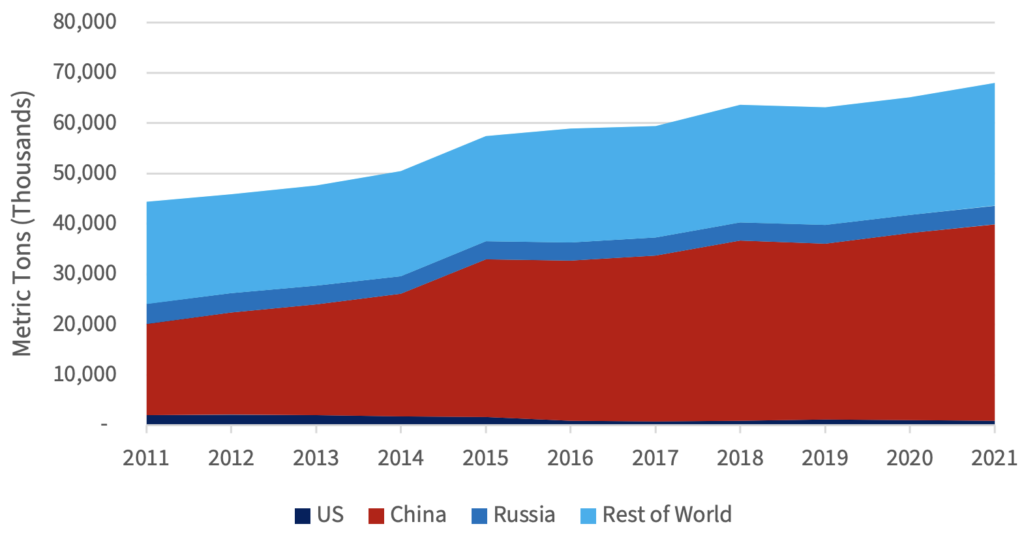

The availability of REEs in the United States has made increased production possible, and Chinese influence over REE markets may decline in the future. But it is unclear if this will be true for other minerals. Figures 5 and 6 below highlight global aluminum and lithium production by country. Note that while global production in both cases has increased substantially, the dominant mineral suppliers remain so. In the example of lithium, in particular, Australia overtook Chile as the largest global producer, thanks to new mines coming online in 2017 and 2018.

Figure 5: Global lithium production.

Sources: USGS Mineral Commodity Summaries 2013-2022 (aluminum and lithium)

Figure 6: Global aluminum production.

Sources: USGS Mineral Commodity Summaries 2013-2022 (aluminum and lithium)

Lithium offers an interesting example of how existing suppliers may be able to increase production due to the existing presence of mineral deposits and further entrench their dominant positions. From 2011 through 2020, global lithium production increased by 170%, led by growth in Australia by 323%, Chile by 100%, and China by 133%. Outside of those producers, the rest of the world doubled their lithium production. For aluminum, the story is much simpler. As a ratio of total global production, China went from being the dominant supplier at 41% of global production to 57%. Over the same period, U.S. aluminum production shrunk from 4% of the world’s output to 1%.

While we can assume that heightened demand for minerals will result in some level of heterogeneity among producers as new production enters the market, we should expect that incumbent producers will remain major suppliers due to favorable geologic conditions.

Refining Concerns

Mineral production is only one aspect of the supply chain; also critically important is the capacity to refine produced minerals. From a conventional economic perspective, refining capacity is a competitive enterprise that is responsive to the market demand for minerals. As demand and production increases, we would expect demand for refining to rise and for new market entrants to satisfy refining needs. In recent years, though, there has been heightened concern that refining capacity may represent a supply chain vulnerability.

For critical minerals, there is the possibility that other countries—especially China—may be attempting to attain increased influence over refining capacity. Currently, China controls 80% of the world’s lithium refining capacity through its state-owned enterprises (SOEs), such as Ganfeng Lithium. In November 2021, Ganfeng signed a three-year contract to supply lithium batteries to Tesla. The SOE is also expanding its investment and control over lithium supplies in other countries, as last year it was approved for a new lithium plant in Argentina.

For lithium production, one would expect Australia to be the most influential player, owing to that economy’s huge lithium production. In practice, however, the multinational investments that flow from Chinese SOEs have enormous influence and control over lithium markets. In terms of a clean energy transition, this power can raise some concerns as to the resource availability of critical minerals, since SOEs do not operate based on market incentives, but rather on the political objectives of their parent nation. Should political divisions arise, it may derail market access to critical minerals.

Concerns about monopoly control over refining are exacerbated when looking beyond lithium. For example, while the DRC produces 68% of the world’s cobalt, it only accounts for 0.1% of the refining. China’s SOEs, meanwhile, are the dominant refiner at 64% of the world’s cobalt refining. Similarly, China produces 9% of the world’s copper output, but controls 37% of the refining capacity.

For example, while the DRC produces 68% of the world’s cobalt, it only accounts for 0.1% of the refining. China’s SOEs, meanwhile, are the dominant refiner at 64% of the world’s cobalt refining.

Recycling

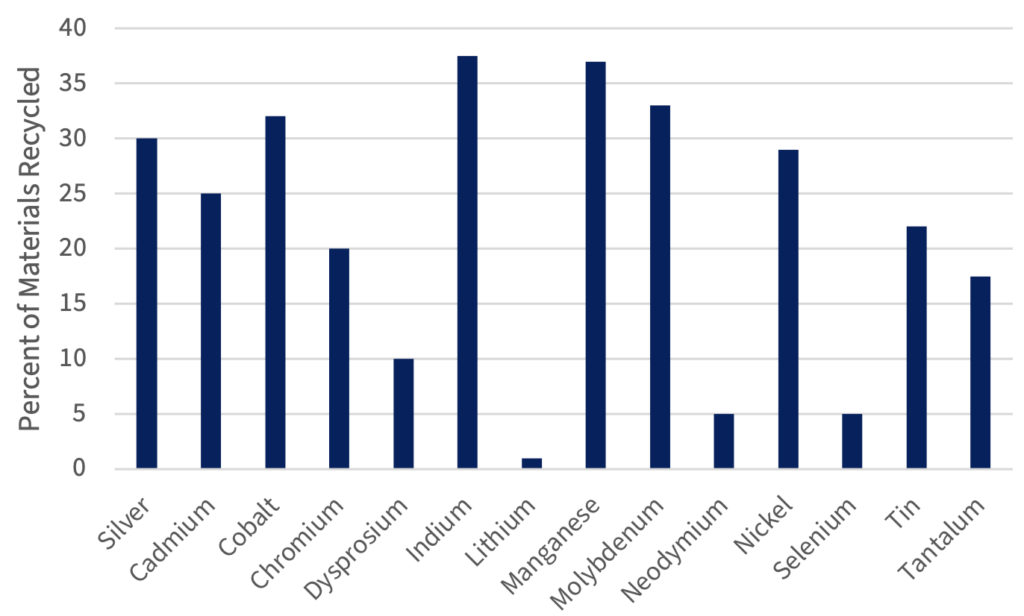

One potential solution to minerals shortages caused by heightened demand for clean energy technology is to dramatically increase recycling. Unlike plastics or other materials, metals typically recycle well because they can be melted and reformed an infinite number of times without losing any of their key characteristics. In Dominish et al., recycling was noted as the single most important policy for improving the achievability of global climate targets with existing technology. But this also raises serious questions as to the current scope of recycling and the achievability of recycling targets. The chart below shows the current recycling rates for critical minerals.

One potential solution to minerals shortages caused by heightened demand for clean energy technology is to dramatically increase recycling.

Figure 7: Current recycling rate

Sources: Valero et al.

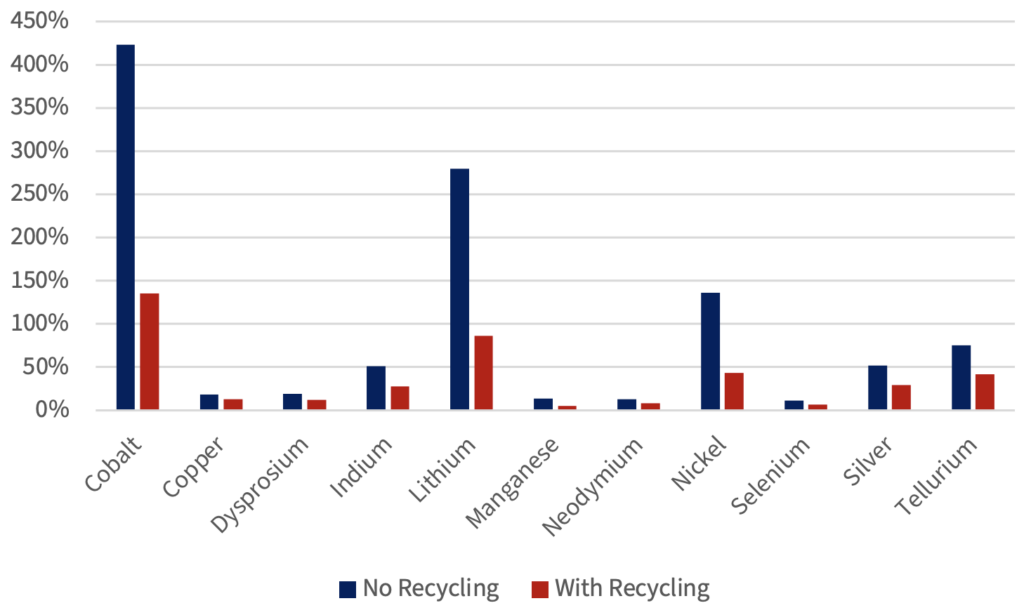

Dominish et al. estimate that recycling can have a significant impact on reducing the demand for minerals. The chart below shows the estimated effect of recycling on total resource demand if 95% recycling rates were achieved, with resource demand expressed as a percentage of global reserves.

Figure 8: Change in mineral demand (% of global reserves)

Sources: Dominish et al.

Dominish et al. show that recycling can have a significant reduction in minerals demand, but it is worth questioning the feasibility of achieving the 95% recycling rate that was outlined in their study. The IEA’s report on critical minerals estimates that recycling will alleviate minerals demand. However, for batteries, the IEA estimates that recycling will only account for 12% of battery minerals supply by 2040.

A major constraint for recycling as a source of minerals for a clean energy transition will be the local waste management policies. Because it is impossible to recycle more than is put in, the challenge with achieving high global recycling rates is that it is not possible for one country to compensate for deficient recycling rates in another, but rather all countries would have to work in concert if extraordinarily high global recycling rates are sought.

Generally, achieving high recycling rates for industrial materials is already incentivized because the high value of the materials, especially in aggregate, creates value for investors. Conversely, achieving high recycling rates of materials that are used primarily by individuals (personal electronics, vehicles, containers, etc.) can be much more challenging because the value of the materials are often low compared to the marginal cost of the behavioral change.

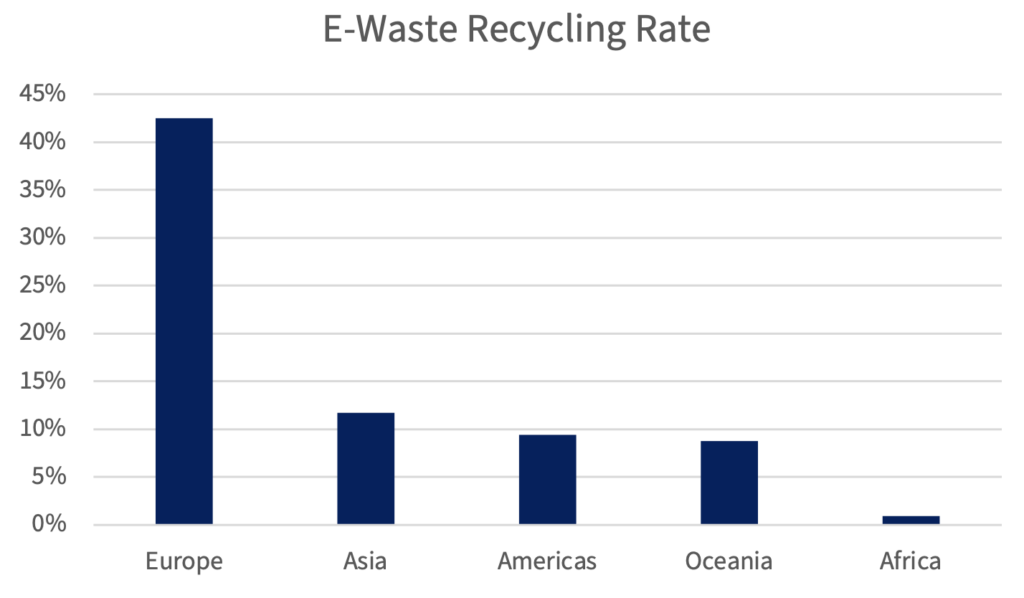

Currently, recycling rates vary substantially by region. Some countries are simply more stringent about their waste management and materials recovery policies than others. As an example, rates for recycling e-waste, which includes critical minerals such as lithium and copper, vary dramatically, with Europe achieving a rate of 42.5%, compared to 0.9% in Africa.

Figure 9: E-Waste Recycling Rate

Sources: The Global E-Waste Monitor 2020

The unfortunate reality is that there is a large disparity in the adoption of recycling and waste management practices around the world. Plastics, in particular, offer a stark example, where high-income nations have near zero percent of their plastic waste inadequately managed, but low-to middle- income nations can have between 80 and 90% of their plastic waste mismanaged. As the push for a clean energy transition and adoption of circular economy principles are predominantly promoted by high-income nations, it is important to note that the conventional recycling culture in high-income nations is not the global norm.

While there is consensus that heightened recycling rates are important to achieving a global clean energy transition, there has not been much policy research on how feasible it is to induce nations globally to dramatically change their recycling practices.

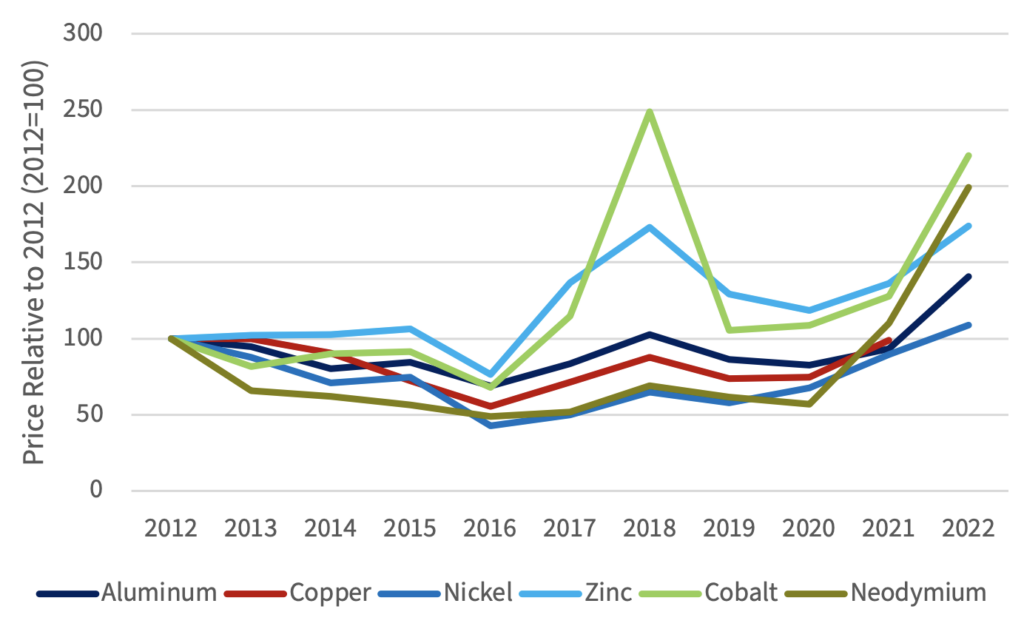

Clean energy demand and minerals pricing

As a fundamental principle of economics, policies that spur demand of a scarce resource will raise the cost of commodities, and thus have a negative impact on consumers. Beyond this simple statement, there is some complexity as the costs of some inputs for a product may rise, but the cost of the product overall can fall due to other factors (e.g., economies of scale, materials efficiency improvements, productivity improvements, etc.). In the case of critical minerals, historical data shows that prices are indeed rising. The chart below shows the price of select critical minerals indexed to January 2012 through January 2022.

Figure 10: Minerals prices.

Sources: Federal Reserve Economic Data; and Trading Economics price data

For the price of critical minerals, there is a risk that widespread adoption of policies that increase the demand for EVs or other mineral-intensive technologies could increase the total cost of reducing emissions and raise the costs of climate action.

It should be noted that impact of higher prices would be manifested heterogeneously, where some countries that benefit from high mineral demand, like China, could see a net benefit, while countries that finance large subsidies or are low-income could experience economic harm. Should this occur, political enthusiasm for a global clean energy transition may be diminished, which could threaten the overall incentives for climate mitigation.

Ethical Concerns with Minerals Production for a Global Clean Energy Transition

There are growing concerns about the ethics of minerals production upstream in the clean energy supply chain. Minerals required for low-carbon technologies are sometimes produced unethically, with child and even slave labor.

Child labor

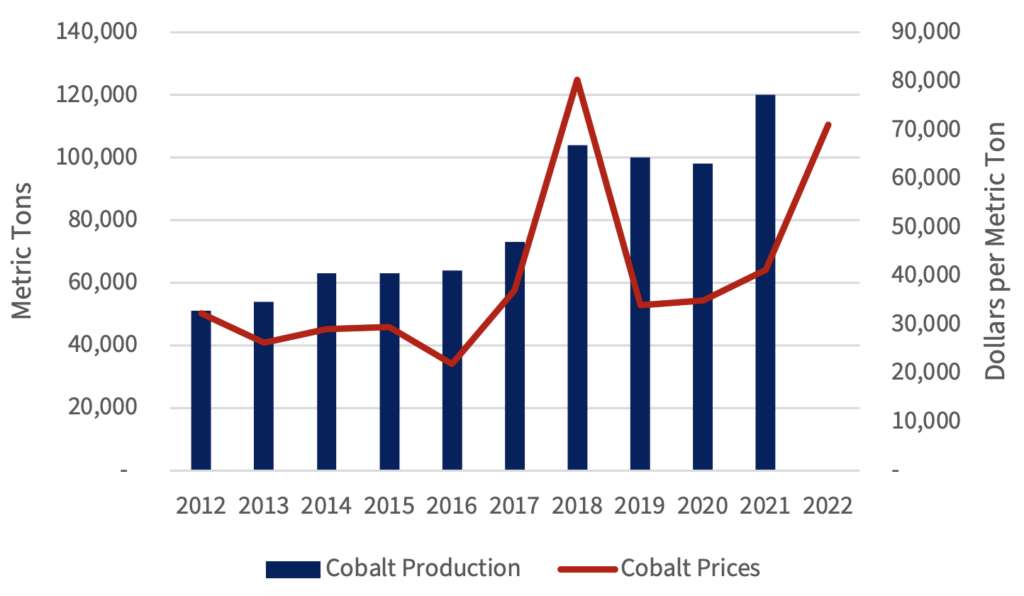

The Democratic Republic of the Congo (DRC) has been found to utilize child labor in its production of cobalt. Roughly 40,000 children aged six and older work in cobalt mining, which is 15% of all cobalt miners in the country. This figure is up from the estimated 35,000 in 2018. According to the U.S. Department of Labor, approximately 36% of children between the ages of 5 and 14 in the DRC are working. These children are typically tasked with sorting, washing, and transporting ore.

As demand for cobalt has risen, especially for EVs, the DRC has increased its production. The chart below shows Congolese cobalt production, as well as cobalt prices.

Figure 11: DRC Cobalt Production and Cobalt Price

Sources: USGS Mineral Commodity Summaries 2022 and Trading Economics cobalt price data

As expected, heightened prices in 2018 spurred increased DRC cobalt production. These rising prices are likely to exacerbate the utilization of child labor. Efforts are currently underway to try and improve accountability of cobalt sourcing, as multiple mining companies are attempting to use blockchain technology to trace the origins of cobalt. However, the complexity of minerals supply chains, where minerals from multiple sources are mixed for smelting, may make it difficult to achieve the hoped-for accuracy.

Slave labor

While it was initially hoped by many proponents of clean energy that its adoption would result in the United States and other Western nations being leaders in global clean energy production, such views failed to account for an understanding of “comparative advantage” in economics. Low-cost suppliers dominate global production for a wide array of products, and clean energy is no exception. In 2019, China was responsible for 80% of the world’s supply of solar panels.

Unfortunately, some Chinese producers achieve their low cost by utilizing slave labor. A key component for solar panels is polysilicon, of which the Xinjiang province in China produces 45% of global supply. A report from Sheffield Hallam University found there is “significant evidence” that the 2.6 million “minoritized citizens” working in “surplus labor” in Xinjiang are in fact slave laborers.

In response to these concerns, the Biden administration has banned imports of silicon products from Hoshine Silicon Industry, a Chinese company suspected of utilizing slave labor. It is not yet clear, however, if alternative producers of polysilicon will arise to ethically satisfy demand for solar panels.

National Security Concerns

In the 1970s, Arab members of the Organization of the Petroleum Exporting Countries (OPEC) embargoed the United States due to its support for Israel in the Yom Kippur War. Consequently, gasoline prices at home quadrupled, and Americans faced a steep recession. In response to this vulnerability, the United States created the Department of Energy, hoping to discover alternative energy sources to mitigate the ability of foreign nations to use their natural resources as a weapon.

Growing reliance on foreign supply chains for U.S. weapons procurements and low-carbon technologies risks undermining the economic and energy security that the United States has achieved in recent years, thanks largely to the shale revolution in oil and natural gas. This threat is unlike U.S. dependence on foreign oil since the effect of an energy supply shock is essentially immediate. However, it creates a scenario where a political or security crisis resulting in a cut-off of foreign mineral supplies could severely curtail domestic production of defense and energy technology products.

In 2010, the notion that critical minerals could be used to punish rival powers transitioned from theory to reality, due to the Senkaku Boat Collision Incident. An altercation between a Chinese fishing vessel and a Japanese Coast Guard vessel in the Senkaku islands (disputed waters, but Japanese administered) resulted in the Chinese government embargoing REE exports to Japan. This is unlikely to be an isolated incident, as the Center for Studies of International Crises and Conflicts at the University of Louvain found that the “Chinese government intends to…grab a monopoly situation on other minerals and elements (such as REEs), or to use its influence as the world leader of the sector over foreign firms.”

Potential concerns about embargoes as tools for achieving political concession have been reinforced with the Russian invasion of the Ukraine in 2022. European dependence on Russian energy supplies has been noted as a reason for the lack of a unified response from Western Europe to Russian aggression. A reliance on a foreign supplies for critical minerals may not in and of itself be a cause for conflict, but creates the potential for foreign powers to raise the costs of a U.S. response to foreign policy issues.

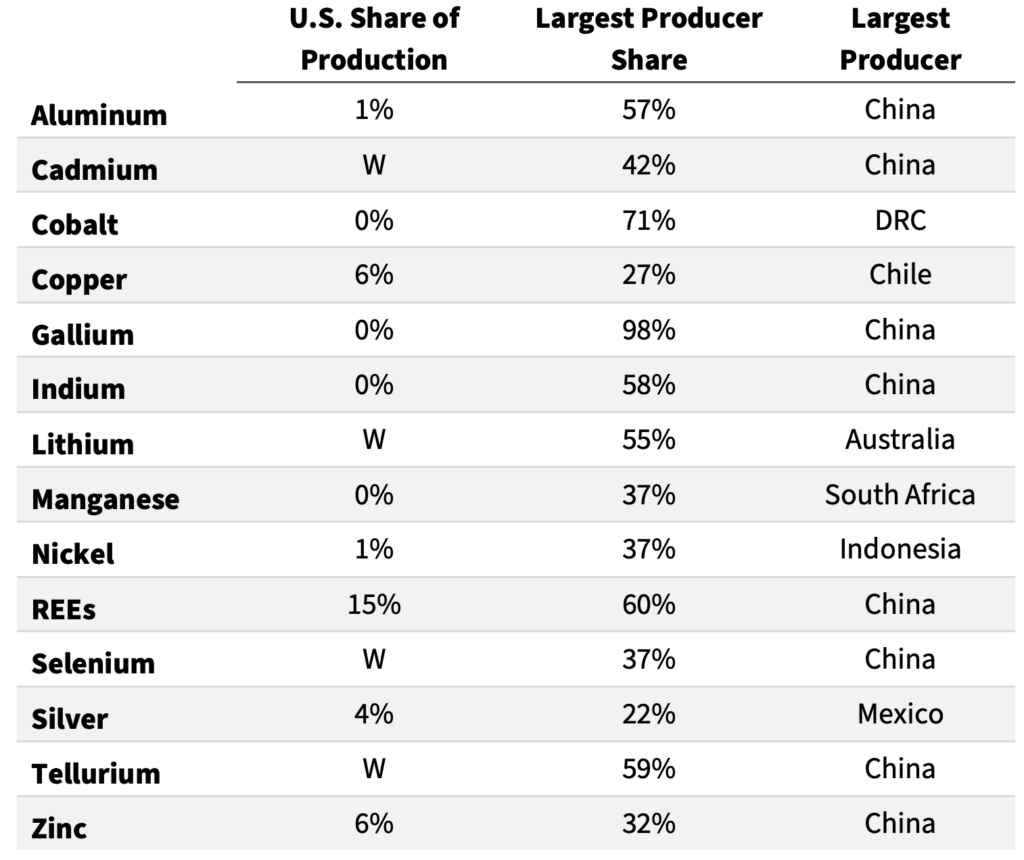

The chart below shows several critical minerals for which there is data, U.S. production of each mineral,

and the world’s top producer and their associated production.

Table 4: Production of various minerals, U.S. share and largest producers. W denotes withheld information.

Sources: USGS Mineral Commodities Summaries 2022. W denotes withheld data.

Of the 14 listed critical minerals, eight of them have China as the world’s top producer. In only one case was U.S. production more than 10% of global supply, which is the case of REEs, thanks to recent increases in domestic production.

The lack of diversity in the minerals supply chain, scarcity of deposits, high demand for minerals for clean energy technology, active expansion of Chinese refining capacity for minerals, and the demonstrated historical willingness to embargo mineral exports to foreign nations all combine to indicate a significant possibility of future security vulnerabilities.

Expanding critical minerals production in the U.S.

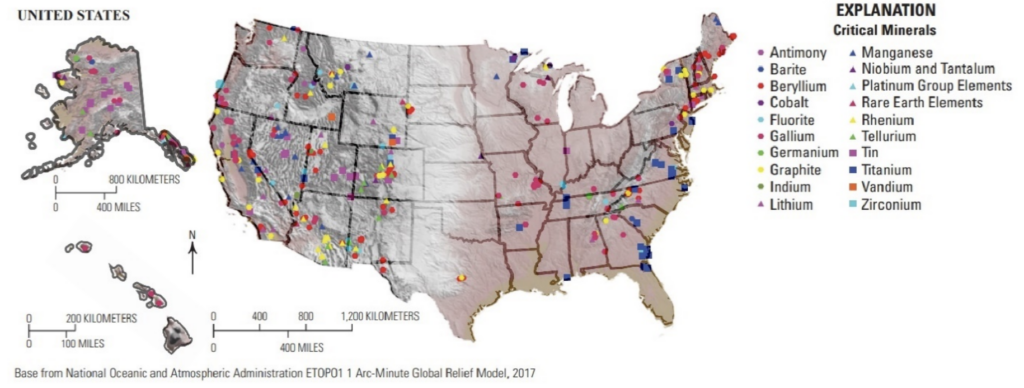

The United States is 100% net import-reliant for 14 critical minerals, and more than 50% import-reliant for 17 other mineral commodities. The Department of Energy states that this dependency could be a problem as a source of risk for U.S. supply chains. Diversifying supply by expanding recycling, exploration, production and refining capacity both domestically and with friendly nations will be crucial for addressing vulnerabilities in the critical minerals supply chain. While United States will not be a world leader in global lithium resources, it does have non-trivial production potential through its 750,000 metric tons of identified reserves and 9.1 million tons of lithium resources. The United States also has 69,000 metric tons of reserves and 1 million tons of resources for cobalt. These resources only represent a fraction of the global total, but do represent untapped opportunities for the United States to supply minerals needed for clean energy technologies.

Figure 12: Location of critical minerals resources in the United States.

Sources: USGS, “United States Critical Minerals Locations,” https://www.usgs.gov/media/images/united-states-critical minerals-locations.

Opportunities for U.S. critical minerals production are sometimes not pursued due to burdensome regulation. In particular, the National Environmental Policy Act (NEPA) requires that “major federal action[s]” like permitting be subject to environmental review. However, research has shown that NEPA is far more likely to negatively impact clean energy-related projects than fossil fuel ones, with 42% of DOE NEPA environmental assessments and environmental impact statements being for clean energy, transmission, or conservation efforts compared to 15% for fossil fuel. Similarly, of all the active environmental impact statements for the Bureau of Land Management 24% were for renewable projects and 13% were for fossil fuels. Because government regulation and permitting does not always consider the net environmental benefits or impacts from projects, they can sometimes have the perverse effect of delaying clean-energy related projects and entrenching reliance on incumbent energy suppliers.

Litigation is the most frequently cited reason for delays related to the NEPA process, and agencies that take longer to prepare NEPA documents are less likely to be sued. In one example, an attempt to construct a lithium mine in Nevada, Rhyolite Ridge, was opposed by environmental groups, citing concerns of biodiversity loss. Despite the proposed facility’s plans to mitigate those risks, the project still is encountering permitting difficulty.

U.S. environmental laws have traditionally focused on minimizing pollution, but they are ill equipped to consider the tradeoffs and potential net impacts from new infrastructure. In the example of Rhyolite Ridge, it may be more prudent to permit the mine and accept the risk to biodiversity to avoid a worse environmental impact from either more constrained EV battery supplies or alternative lithium suppliers. Nonetheless, processes to evaluate as much are not in place—a problem that should be addressed through regulatory reform or modernization.

Reducing the demand for critical minerals

Because modelers can only assume that the technology available today will supply clean energy in the future, they ignore the possibility for breakthrough innovations to circumvent the need for critical minerals. Consequently, estimates of the mineral requirements for a global clean energy transition end up being enormous, but improvements in technology could mitigate these impacts.

Breakthrough technology improvements could dramatically alter global reliance on select critical minerals. For example, the development of low-carbon, drop-in replacement liquid fuels for ICEVs, such as those produced with artificial photosynthesis, would substantially reduce the demand for EV batteries. Similarly, breakthroughs in carbon capture technology, such as the zero emission Allam cycle for natural gas electric power generation, would significantly reduce the need for wind and solar power generation as existing supplies of natural gas could produce zero emission electricity.

Achieving breakthrough innovation will require policies that seed innovation, as well as maintaining an open market that allows new entrants to compete. Tax credits, tax advantaged financing, grants, and programs like ARPA-E can all help in ensuring that early stage, not-yet proven technologies have market opportunities. More important, though, is market design. If policymakers deem that all energy should come from specific sources, as has happened in several states, they are precluding market entry of new low- or zero-carbon technologies that may not fit the envisaged clean energy future.

Ultimately, policymakers need to preserve opportunities for competition and market dynamism, so that if better, lower-cost clean technologies emerge, those new industries can displace incumbents. This will be especially important if minerals prices continue to rise, as would be expected if major economies begin adopting clean energy mandates.

Sanction unethical minerals suppliers

While the United States has implemented sanctions on Chinese companies over slave labor concerns regarding polysilicon, there should be a broader, more concerted effort to eliminate unethically produced minerals from the global supply chain. Absent a concerted effort to clamp down on bad behavior now, the United States could eventually end up in a position where major portions of its incumbent energy infrastructure are reliant on unethically produced minerals, at which point the domestic cost incurred by sanctions would be significantly higher. Consequently, the United States and its allies can curtail reliance on unethically produced critical minerals before it becomes too late.

Verification of ethical production can be better pursued, and policymakers should consider withholding U.S. subsidies for EVs or renewable energy to companies that cannot transparently prove they do not rely on unethically produced minerals. The West should also actively pursue sanctions against Chinese and Congolese companies that are suspected of utilizing slave or child labor. The high price of minerals has increased the incentive for bad practices in their production, and as a major consuming market, the United States is best positioned to effect change by refusing market access to unethical suppliers.

Conclusion

A global clean energy transition utilizing existing technologies like EVs and renewable electricity is an extraordinarily minerals-intensive proposition. There is only limited available research as to the totality of minerals that would be required for achieving such efforts globally, but what research has been conducted shows mineral requirements that are commonly in excess of 25% of global reserves for some resources, and in some cases even greater than 100%. It is expected that the extraordinary demand for minerals will put upward pressure on prices, exacerbating the costs of an energy transition that is already expected to be very expensive.

Concerningly, the vast majority of critical minerals in both production and refining capacity is controlled by only a few nations, particularly China. Policies that increase reliance on foreign supply chains could create national security vulnerabilities, as China has already in the past expressed willingness to embargo mineral exports to penalize foreign nations.

There are also growing ethical concerns with the production of minerals. A significant portion of Congolese cobalt miners are children, and the largest source of polysilicon for solar panels in the world is a region in China utilizing slave labor. While there have been modest responses to these problems, they are worsening rather than being alleviated.

The U.S. policy response to these issues has been deficient. The political appeal of pursuing renewable energy growth at any cost is potentially precluding opportunities for breakthrough innovations that are less minerals-intensive and more likely to be sustainable. Domestic laws for environmental protection are ironically preserving incumbents rather than creating opportunities for increased domestic minerals production that could expand clean energy growth.

In recognizing that the availability of critical minerals presents a key constraint for widespread adoption of existing clean energy technologies, the United States should expand its pursuit of clean energy innovations that may prove more sustainable in the long term, as well as advanced recycling programs. In the interim, the United States should also increase its own minerals production and processing to reduce the influence of China and other geopolitical adversaries. Should the United States not adopt these practices, it risks a similar situation to the 1970s where reliance on adversarial regimes for key commodities results in an economic liability that would be exploited to the nation’s detriment.